However, the past two years have made me realize that Hubbert's Peak may have passed for conventional oil only, not for all oil. Supply finally caught up with and passed demand, causing oil prices to fall, both of which fit the predictions of mainstream economics. Too see both the increased supply and the lower price, first look at this graph of world oil production from Econbrowser. The blue line shows the period of the "bumpy plateau" that looked like the one predicted from Peak Oil theory.

Compare with this graph showing the price of West Texas Intermediate (WTI) and Brent Crude from Calculated Risk.

That bump in production above the blue line during the past three years coincides with the drop in price. That's the good news out of all this.

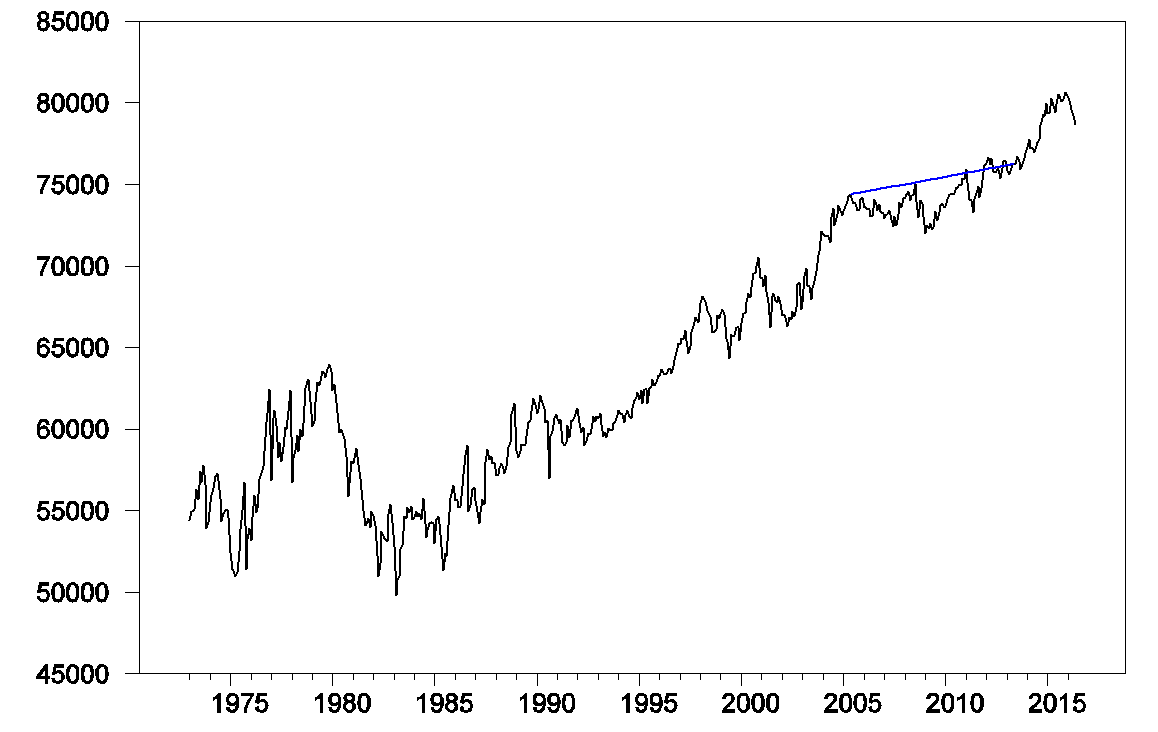

The bad news is the other side of supply and demand. When prices fall, supply eventually falls as well. I've been expecting that to happen since December 2014. The graph below from Econbrowser shows that it has happened, at least for the U.S.

As a result, U.S. and world production is falling again, so the prices have resumed rising. Calculated Risk's graph of year-over-year oil prices shows that prices are actually slightly up from a year ago for the first time in more than two years.

The result at ground level is that the downward seasonal pressure on gas prices at the pump is being counteracted by upward pressure from wholesale prices. I saw that yesterday, when I filled up at one of the stations in my old neighborhood, which was selling regular at $2.27. Two weeks ago, it was selling regular for $2.10. The first time I visited the station in August, I bought regular for $2.09. That's a graph of slightly increasing prices when the usual trend is for falling ones. Fortunately, prices are still relatively low and I drive a Prius, so I'm not complaining in earnest, as it could be and has been a lot worse.

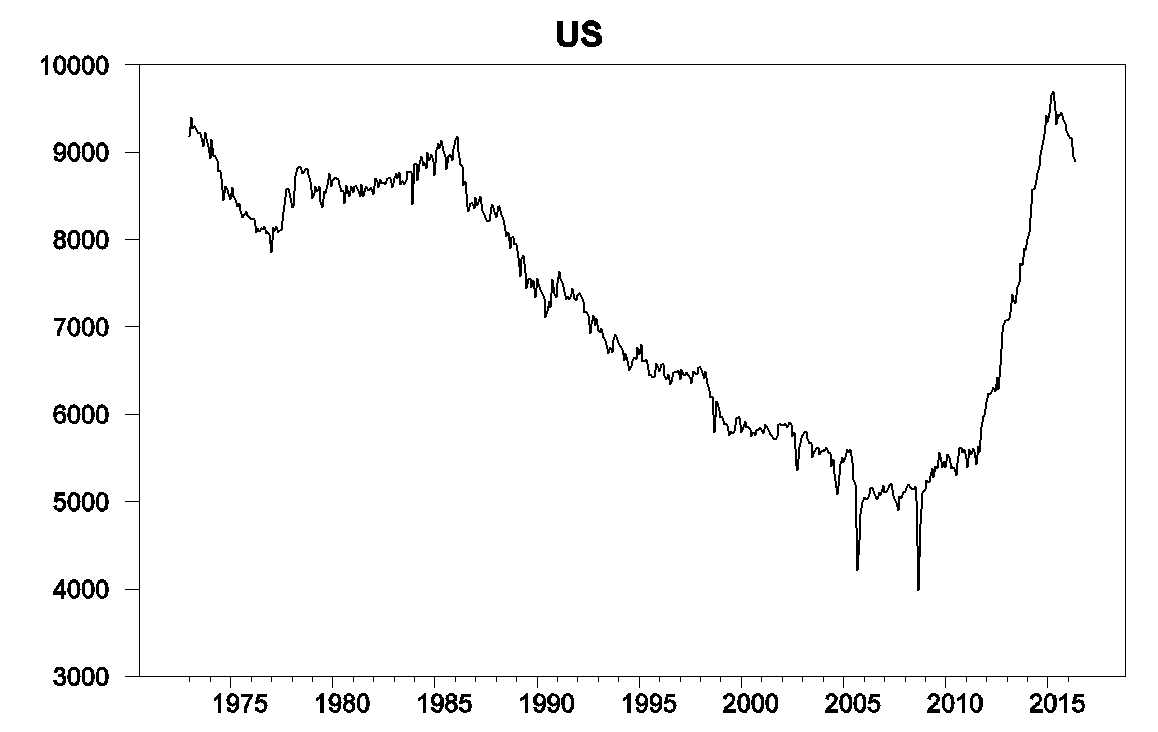

Another result of the oil price drop that I feared would be financial chaos from the shale oil bubble bursting wiping out the gains to the consumer economy from lower energy prices. That didn't happen, but trouble with shale oil did counteract the improved situation for the consumer, as this graph from Econbrowser shows.

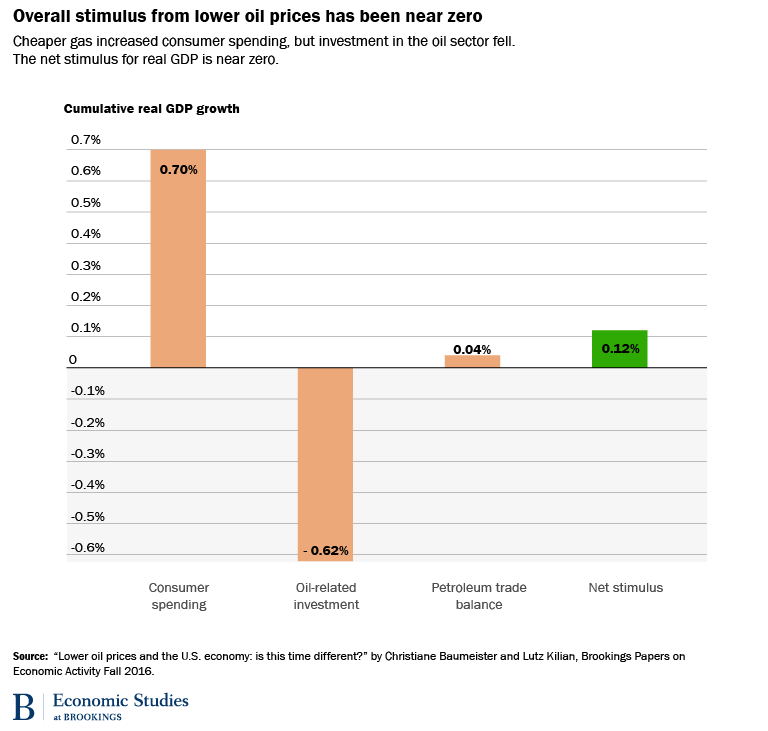

GDP improved from lower oil prices, but only 0.12% worth. James Hamilton explained the situation thus.

But gains to consumer spending were mostly offset by a drop in oil-related investment spending. Nonresidential fixed investment had been growing at a 4.3% rate prior to the oil-price drop but has only increased at a 0.8% annual rate since, due to a 50% drop in investment spending in the oil sector.As for my prediction of a recession starting sometime in 2017, I'm even more confident than before. Now that oil prices are rising, the possibility of an oil-price-shock has increased, especially with this news from Bloomberg: OPEC Agrees to First Oil Output Cut in Eight Years. If OPEC succeeds in getting Saudi Arabia, Iran, and Iraq on the same page on this, further price increases are inevitable. If they exceed 50% in one year, so is the oil-price-shock recession.

The U.S. imports 6 million more barrels of crude petroleum and refined products than it exports every day. Between June 2014 and March 2016 the real price of oil declined by 68%. As a net oil importer, the fact that Iraq and Iran are now willing to sell us more oil at a lower price should be good news for the U.S. economy. In idealized economic models, the resources that had been producing oil should now shift to producing other goods, and with the new terms of trade we should as a result be even more productive than before.

But in the real world shifting resources is easier said than done. We now have a large stock of capital that was being used to develop U.S. shale oil, and contrary to the predictions of simple economic models, there is not some other more productive place to use that equipment.

This comment has been removed by a blog administrator.

ReplyDeleteAs I've written before, I will delete this spam on sight.

Delete