Last month I forecast the future of the multi-year increase in miles driven by Americans that "I expect this trend to continue until the next recession, which I'm still predicting will begin next year. I'll re-evaluate my forecast next month. Stay tuned." Not only is next month now this month, it and the year it is part of are already almost over, so it's time for me to follow through before my promise turns into a pumpkin at the stroke of midnight on New Year's Eve. Revising my economic forecast has become especially important in light of the passage of the tax "reform" bill, which I didn't think I'd include at the start of November.

First, it's time to revise the recession outlook from what I wrote at the end of June.

The lower gas prices, continuing low unemployment rate, and near-record-high stock indices all suggest that the U.S. economy is not headed for recession in the next six months. I'm delaying my prediction by one Friedman Unit, which is six months, so the deadline for the U.S. heading into recession is now one year from tomorrow [June 30th]. Enjoy the expansion while it lasts.While gas prices are up year over year and U.S. crude oil closed above $60/barrel for the first time in nearly three years, the unemployment rate is still very low and the Dow Jones Industrial Index is just off the 70th record high of the year. Along with other factors, it looks like the onset of the next recession is still more than six months off. Consequently, I'm postponing my call for it to begin for another five or six months, until next November or December. Since it takes two consecutive quarters (six months) of decreased Gross Domestic Product (GDP) for a recession to be declared, no one will know for certain until July 2019. Enjoy not officially being in recession for more than a year.

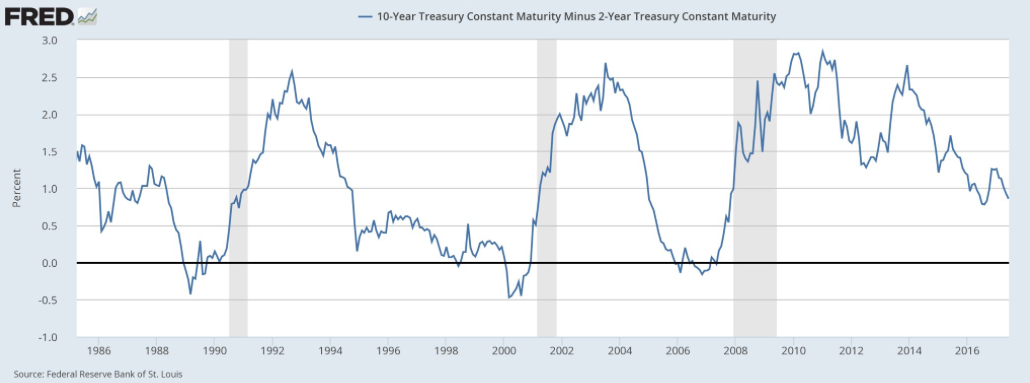

Three things could trigger the next recession. The most likely would be an inversion of the yield curve, which means that short-term interest rates would rise higher than long-term interest rates. The Federal Reserve has been raising short-term rates for the past two years while long-term rates have been rising much more slowly. If present trends continue, short-term rates will rise above long-term ones within a year or two, which always signals a recession within a year. See the graph below. When the black line is below zero, the yield curve is inverted. That is always followed by a gray bar, which marks a recession.

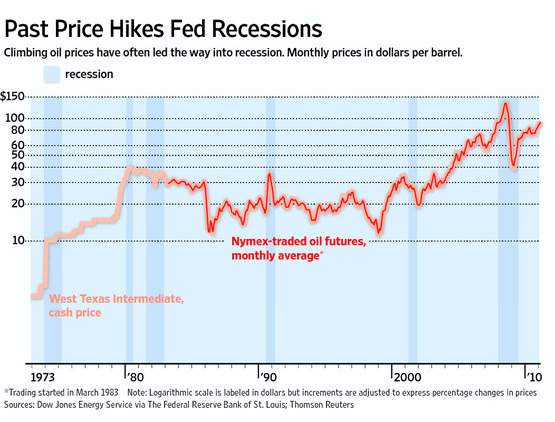

The second is a rapid rise in oil prices, which has occurred either slightly in advance or concurrently with every recession since 1973. Again, see the chart below, which shows that relationship and in which the shaded bars represent recessions.

The last, which the U.S. saw along with both of the above during the last recession, would be a crash in housing prices. However, that is not as reliable an indicator of contraction, as it took nearly two years between the bursting of the housing bubble and the onset of the Great Recession of 2008-2009, barely happened before the recession of 1990-1991, and it didn't happen at all before the 2001 recession, all of which the graph below shows.

Keep all three of these in mind when I analyze the effect of the tax bill on the economy.

Before I do, I want my readers to notice the timing of recessions. They range from seven (2001 to 2008) to eleven years (1990 to 2001) apart. That range is exactly consistent with the Juglar Cycle, an economic cycle that lasts seven to eleven years, the downturns of which correlate to U.S. recessions since 1980. The Great Recession technically began in December 2007 and adding eleven years to that means the next one should start no later than December 2018. We're due.

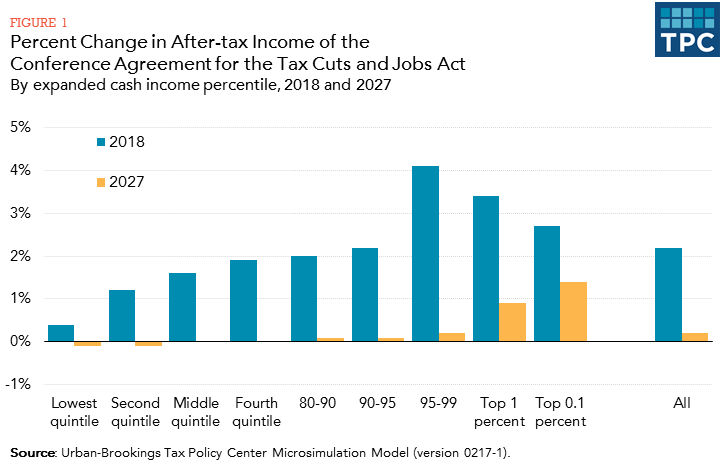

Now it's time to examine the effects of the tax bill on the economy. I begin by saying that I doubt it will speed up the next recession or make it worse overall, although I can imagine some ways it could do either or both. What's more likely is that the law's effects will make things worse for some people, while actually having a slight positive effect on others. What the new tax regime will make much worse is not the recession that's coming next year and the year after next, but the recession after that in the mid to late 2020s, when the temporary tax cuts expire, income inequality is much worse, and the nation is more in debt. To explain all of my projections, I'll refer to the graph below.

The blue bars show that almost everyone will have more money to spend beginning next year and ending in 2026. In the short term, that will create more economic growth as people spend their after-tax income. During a recession, that will soften the impact of a slowing economy, just like the Bush tax cuts were one of the factors that helped make the 2001 recession rather mild. In fact, I expect the next recession to be somewhere between the 2001 recession or the 1990-1991 recession in its effects, probably closer to 2001. Before then, the extra disposable income runs the risk of overheating an already booming economy, never mind that the fruits of that economy are very inequitably distributed. That will increase demand for oil and other energy sources, making their prices go up. That will cause inflation to rise again as energy costs become distributed throughout the economy. Higher inflation will prompt the Federal Reserve to raise short term rates, eventually inverting the yield curve. Viola, recession!

Now, I won't blame the tax cuts for this. All of this is going to happen anyway; the tax cuts might marginally speed up the process and make it more acute. It might make the difference between the recession starting in November or December of 2018. I already have that covered in my prediction.

What about real estate? Won't the limiting of the deductions for mortgage interest and state and local taxes have an effect on the value of people's homes? Bill McBride of Calculated Risk answers that as the first of his questions for 2018: Will the New Tax Law impact Home Sales, Inventory, and Price Growth in Certain States?

My sense is the low end of the housing market will be fine. The Mortgage Interest Deduction (MID) will be capped at interest on a mortgage up to $750,000 instead of $1,000,000, so the lower priced markets will not be hit by the reduction in the MID. There might be some additional taxes for these buyers due to the limits on SALT and property taxes, but this should be minor.I trust McBride on real estate, so I agree with him on this. Overall home appreciation will slow but not reverse as a result of the tax changes and the effect will be felt mostly by comfortable to well-off but not really rich people in high-tax states. This will upset them, but it won't make them significantly poorer. I expect it will have more of a political effect than an economic one, as many of these people are longtime suburban Republicans in blue states that the Democrats will target to flip next year. Many of them will, voting out Republican Representatives in states like California, New Jersey, and New York.

I also expect the high end of the market to be fine. The high end is already doing well even with the MID capped at $1 million. For these buyers, the bigger impact will be the SALT and property tax limitations, but there will be offsets for these buyers due to the lower rates - and these buyers will likely benefit from the corporate tax cuts. Many of these buyers will also benefit from the changes to the Alternative Minimum Tax (AMT).

It is the upper-mid-range in the certain markets that will probably slow. This might be in the $750,000 to $1.5 million price range. These potential buyers probably don't benefit from the AMT or corporate changes, but they will likely be hit by the SALT and property tax limits.

There could be a ripple effect. If the upper-mid-range slows, that could impact some of the purchases in the next higher range. This is my current guess on the impact.

Some readers may have noticed that I did not mention the stock market as a leading indicator of a recession. That's because, as this Bloomberg View article that tells its readers not to do what I'm doing now notes, "The old joke is that the stock market has predicted nine out of the past five recessions." That's because the stock market will drop and not forecast a recession. For example, the 1987 crash was too far out to predict the 1990 recession. On a related note, the same article also stated that "The stock market was actually up during half of the past 14 recessions." In other words, the stock market may not give a signal at all, just like the housing market did not for the 2001 recession. On the other hand, the article notes "Since World War II, 10 out of the 12 recessions saw the S&P 500 go into a bear market in plus or minus 12 months around an economic slowdown." It's that "plus 12 months" that also makes the stock market not reliable. It may not forecast a recession, just respond to one.

All of that aside, here is how I expect the new tax code will affect stocks. As the both the first and last graph above show, most of the benefits of the lower tax rates and other changes go to the very richest people. Those few million people are not going to spend most of their gains; they're going to invest them. The result will most likely be speculative bubbles that crash the economy when they burst. There may not be enough time for that to have much of an effect before the next recession, but I expect the Dow Jones Industrials to get above 25,000, struggle to break 26,000, then sink down to between 20,000 and 22,500 over the next couple of years. Instead, it will be the next bull market that will feel the full effect of more money from wealthy investors. That's when expect a really big run-up in assets such as stocks, bonds, and real estate followed by a really big crash.

It will be just about that time that the temporary tax cuts will expire. Remember, recessions are tied into the Juglar cycle, which is seven to eleven years long. Seven years from 2018 will be 2025. Eleven years will be 2029. The tax cuts will expire exactly in the middle of that span in 2027. Just as the economy will require more spending, the yellow bars on the graph above show that Americans' after-tax income will decrease, making things even worse. In fact, the bottom forty percent of Americans will have less disposable income than now and the next forty percent will be where they are now. Only the top twenty percent will be better off than in 2017. Decreased consumer spending will make any recession happening then more severe. I expect that contraction to range in severity between the 1974 recession and the 1980-1981 double-dip recession, the third- and second-worst downturns after World War II.

As for the actions of government other than taxes, they could also make recessions worse. Both the deficit and national debt will be larger, making it less likely, but not impossible, for the federal govenment to increase deficit spending to counteract lower consumer spending and investment by business. That might not be as big a deal during the recession coming up this decade, when people will have enough credit available to spend if called upon. That's what happened in 2001, when President Bush didn't actually say, but people still heard, "go shopping or the terrorists win." It will be a problem next decade, when the speculative bubble will cause people to over extend their credit, much like 2007-2009. In addition, any cuts to Social Security, Medicare, and Medicaid, along with pressure on state and local governments to cut budgets because of the loss of the state and local tax dedcution, will also reduce spending among the bottom half of Americans, further depressing the economy.

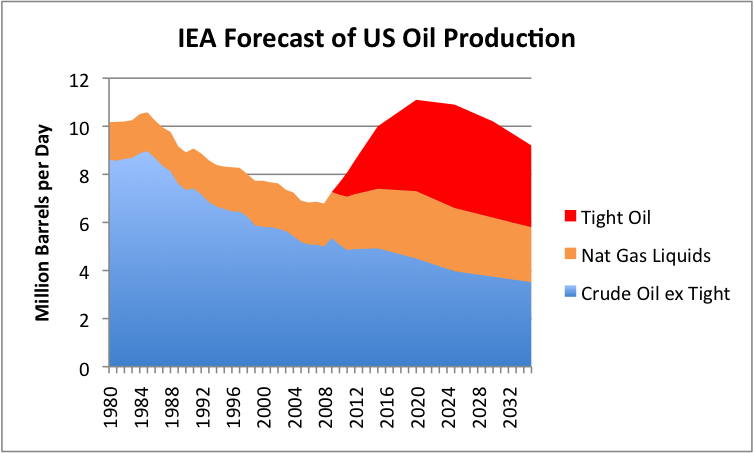

Here's another item to consider, the likely price of oil. The graph below depicts the forecast for oil production in the U.S. Beginning in 2020, it's predicted to decline. That will cause oil prices to increase from 2021 to 2029 unless more oil is imported, which will reduce GDP as the money leaves the country, or Americans decrease their consumption. That will trigger more inflation, which will cause the Federal Reserve to raise rates and invert the yield curve again as well as put pressure on consumer spending. The result will be another recession, which, because of higher oil prices in addition to all the other factors I've already mentioned, will be worse than the one coming up. As Mark Twain said, history doesn't repeat itself but it certainly does rhyme.

With all that in mind, farewell to 2017 and a Happy 2018, even if I think it will start to go bad at the end.

P.S. I wrote this post for Coffee Party USA and a version of it will be posted to their (our, since I'm a director) website. I'll post the link when it becomes available. Stay tuned.

ETA: Also, please read ‘Star crossed lovers’ circa 2018: are revenues and expenditures the Romeo and Juliet of our time? It was written by another director of Coffee Party USA. She has served as the Treasurer of our organization and she applied her fiscal expertise to the tax bill.

ETA 2: Chappelle to poor whites: Trump is fighting for me, not you (VIDEO) is the next in the series of posts written by directors of Coffee Party USA about the tax cut bill. Again, please read.

Thanks for the analysis. I posted a link on my blog with my own two cents - OMFG WE GONNA DIE - about your recession concerns. ;)

ReplyDeletehttp://noticeatrend.blogspot.com/2018/01/the-next-recession-not-matter-of-when.html

Welcome back and thanks for quoting and linking to this entry. I'll leave a comment on your blog later today. I might find that hard cider for you.

Delete